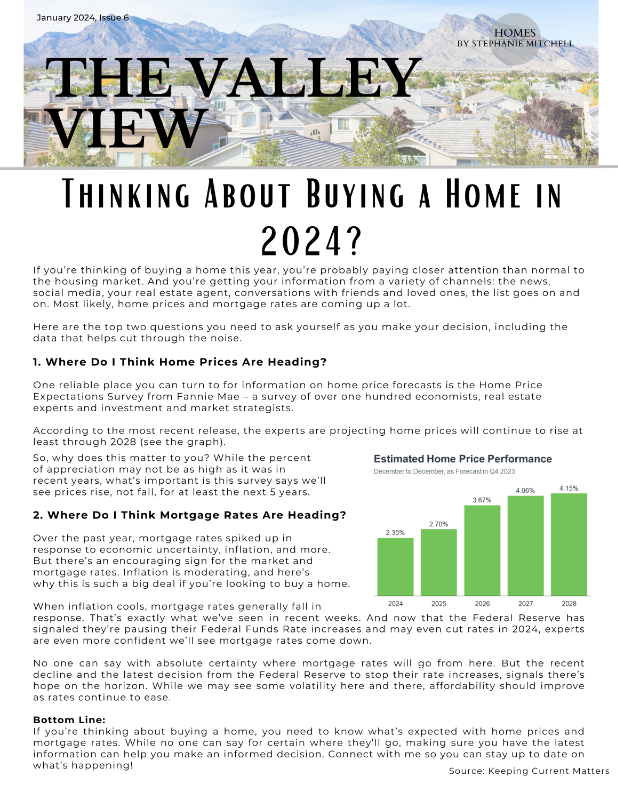

If you’re thinking of buying a home this year, you’re probably paying closer attention than normal to the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot. Here are the top two questions you need to ask yourself as you make your decision, including the data that helps cut through the noise. 1. Where Do I Think Home Prices Are Heading? One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts and investment and market strategists. According to the most recent release, the experts are projecting home prices will continue to rise at least through 2028 (see the graph). So, why does this matter to you? While the percent of appreciation may not be as high as it was in recent years, what’s important is this survey says we’ll see prices rise, not fall, for at least the next 5 years. 2. Where Do I Think Mortgage Rates Are Heading? Over the past year, mortgage rates spiked up in response to economic uncertainty, inflation, and more. But there’s an encouraging sign for the market and mortgage rates. Inflation is moderating, and here’s why this is such a big deal if you’re looking to buy a home. When inflation cools, mortgage rates generally fall in response. That’s exactly what we’ve seen in recent weeks. And now that the Federal Reserve has signaled they’re pausing their Federal Funds Rate increases and may even cut rates in 2024, experts are even more confident we’ll see mortgage rates come down. No one can say with absolute certainty where mortgage rates will go from here. But the recent decline and the latest decision from the Federal Reserve to stop their rate increases, signals there’s hope on the horizon. While we may see some volatility here and there, affordability should improve as rates continue to ease. Bottom Line: If you’re thinking about buying a home, you need to know what’s expected with home prices and mortgage rates. While no one can say for certain where they’ll go, making sure you have the latest information can help you make an informed decision. Connect with me so you can stay up to date on what’s happening!

Create an Account

Search the MLS and featured property listings in real time.